Sealaska Settlement Trust FAQs

Monday, April 4, 2022

![]() Sealaska shareholders approved a resolution to establish the Sealaska Settlement Trust by a margin greater than three to one during the 2021 shareholder election.

Sealaska shareholders approved a resolution to establish the Sealaska Settlement Trust by a margin greater than three to one during the 2021 shareholder election.

The trust frees Sealaska shareholders from paying federal income tax on their dividends. It will also reduce Sealaska’s tax obligation to the federal government in the future.

The trust frees Sealaska shareholders from paying federal income tax on their dividends. It will also reduce Sealaska’s tax obligation to the federal government in the future.

Sealaska will work to ensure the trust is accountable to shareholders and has created processes and policies that aim to maximize the benefits we can offer shareholders. Please read on for answers to frequently asked questions about the Sealaska Settlement Trust.

“Settlement trusts have been widely used by Native corporations since the 1990s. They are a proven tool,” said Sealaska President and CEO Anthony Mallott. “We are excited to roll out this new approach to distributions because we know it will bring valuable savings to our shareholders.”

THE BASICS

Why did Sealaska establish a settlement trust?

An Alaska Native Corporation settlement trust provides Sealaska shareholders with significant tax advantages.

Distributions to shareholders (referred to as “beneficiaries” under the trust) are no longer subject to federal tax. Changes to federal tax law in 2017 allow Native corporations to make contributions to a settlement trust using pre-tax dollars. This change reduces the federal government’s share of a Native corporation’s income, creating a cash savings that can then be used to fund benefit programs, like distributions.

What is a settlement trust?

Under the Alaska Native Claims Settlement Act (ANCSA), Sealaska can set up a special entity called a “Settlement Trust” that is legally separate from Sealaska and dedicated to providing benefits to shareholders and descendants. The purpose of a settlement trust is to provide for the health, education, cultural preservation and economic welfare of Alaska Native people and descendants who are the “beneficiaries” of the settlement trust.

In the past, Sealaska paid dividends to the shareholders directly. Now, Sealaska transfers money to the settlement trust, which is used to make distributions to shareholders.

I heard about the new Sealaska Settlement Trust. Where do I sign up?

There’s no need to sign up for anything or fill out any paperwork. Shareholders retain their shares in Sealaska, and are now also beneficiaries of the Sealaska Settlement Trust in equal proportion to the shares they own in Sealaska. For example, a shareholder who owns 100 shares in Sealaska now owns 100 units in the Sealaska Settlement Trust as well. Your distributions will be paid to you as usual and the experience should be seamless.

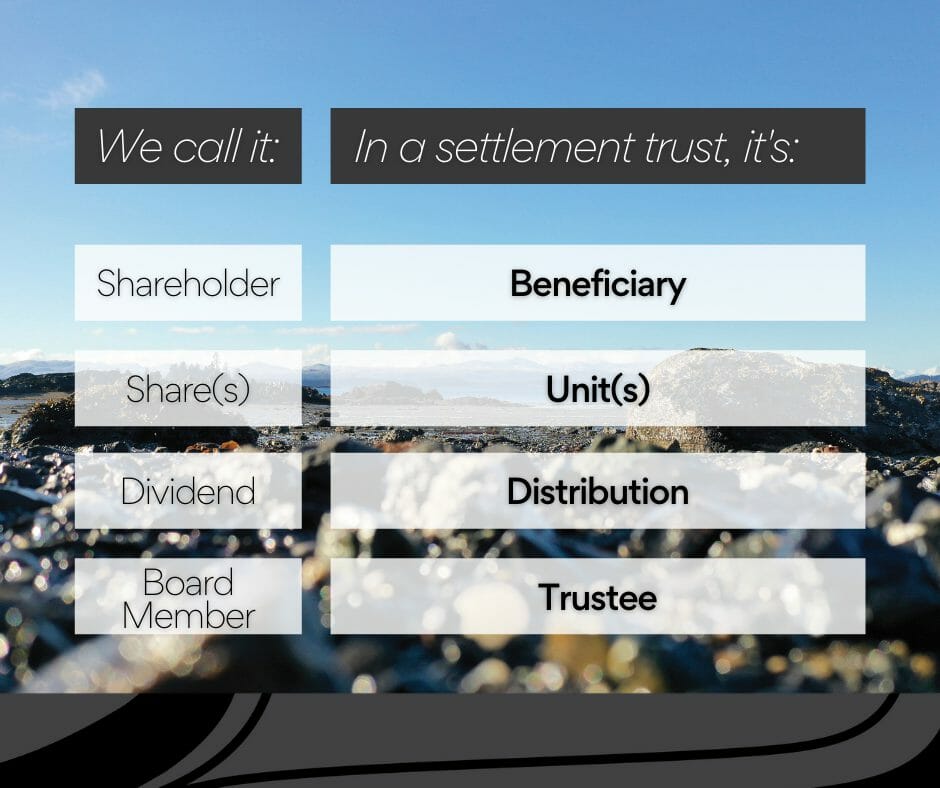

Common Terminology Associated with a Settlement Trust

Settlement trusts use different words for many of the concepts you’re familiar with as a shareholder or descendant of Sealaska.

What does “tax-free distributions” mean?

Shareholder distributions made through the settlement trust are not subject to federal income tax.

Shareholders may still have to pay state tax, though. In Alaska and Washington, where the vast majority of our shareholders reside, there is no state-levied personal income tax, so distributions from the settlement trust will be 100% tax free. Elsewhere, distributions could be taxed if the state where you live has personal income tax.

Shareholders of class A, B, and C shares will continue to receive ANCSA Section 7(j) distributions either directly from Sealaska or their village corporation and those amounts will still be taxable.

When did it go into effect?

Shareholders received their first distribution via the trust in the fall of 2021. The second trust distribution is scheduled for Friday, April 22.

How long have ANCs been using settlement trusts?

Settlement trusts are not new. They have been used by Native corporations in Alaska since the late 1980s and have been approved by shareholders of Ahtna Inc., Bering Straits Native Corporation, Calista Corporation, Cook Inlet Region Inc. and NANA Regional Corporation, along with many village corporations in our region including Goldbelt, Inc., Kootznoowoo, Inc., and Huna Totem.

In fact, Sealaska already has an established Elders’ Settlement Trust for one-time payments to shareholders of Class A, B and C stock when they reach the age of 65. The relatively new tax law, however, allows Sealaska’s new settlement trust to benefit all Sealaska shareholders and descendants year after year.

Latest News

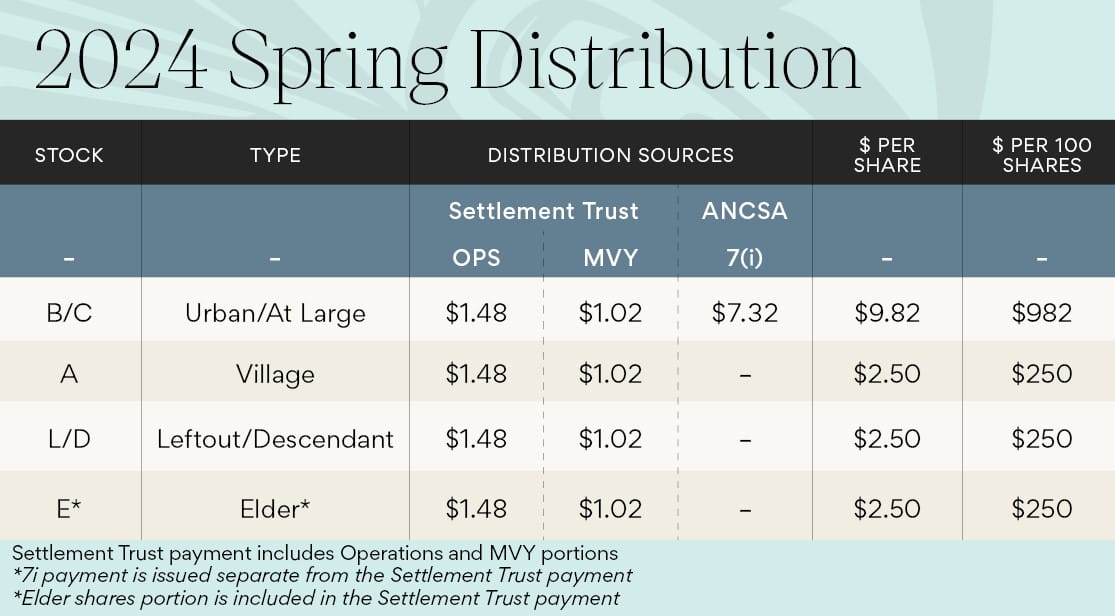

Sealaska Announces Spring Distribution of $19.2 Million

Posted 4/12/2024

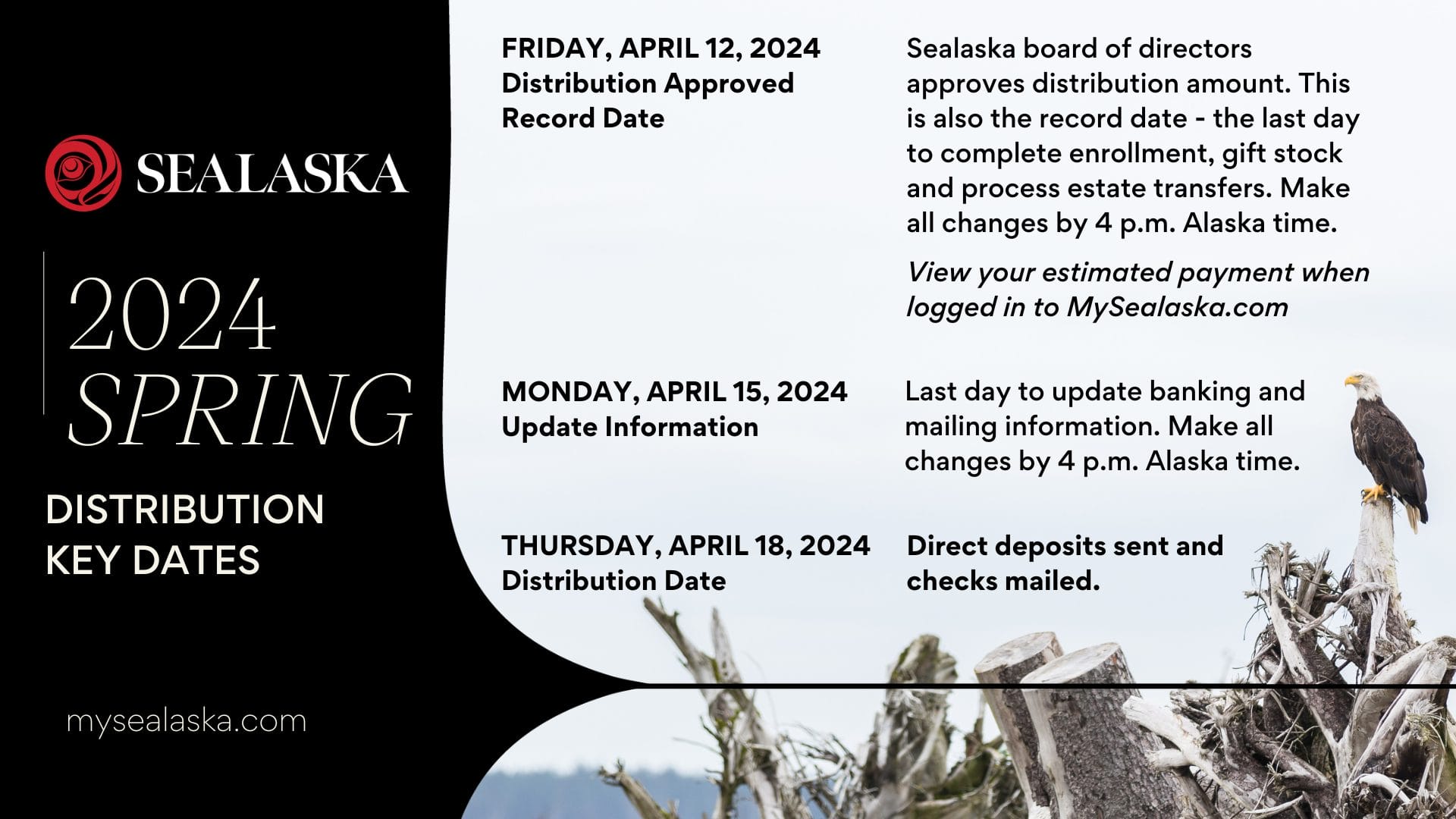

Sealaska Spring 2024 Distribution Date Announced

Posted 3/19/2024

Sealaska announces Desiree Jackson to serve as Vice President of Administration and Outreach

Posted 3/6/2024

First Quarter Board Q&A provides shareholders an opportunity to connect with their board

Posted 3/4/2024

Virtual Shareholder Orientation offers connection, information for original and new shareholders alike

Posted 2/26/2024