Sealaska Settlement Trust FAQs

Monday, April 4, 2022

Sealaska shareholders approved a resolution to establish the Sealaska Settlement Trust by a margin greater than three to one during the 2021 shareholder election

The trust frees Sealaska shareholders from paying federal income tax on their dividends. It will also reduce Sealaska’s tax obligation to the federal government in the future.

Sealaska will work to ensure the trust is accountable to shareholders and has created processes and policies that aim to maximize the benefits we can offer shareholders. Please read on for answers to frequently asked questions about the Sealaska Settlement Trust.

“Settlement trusts have been widely used by Native corporations since the 1990s. They are a proven tool,” said Sealaska President and CEO Anthony Mallott. “We are excited to roll out this new approach to distributions because we know it will bring valuable savings to our shareholders.”

THE BASICS

Why did Sealaska establish a settlement trust?

An Alaska Native Corporation settlement trust provides Sealaska shareholders with significant tax advantages.

Distributions to shareholders (referred to as “beneficiaries” under the trust) are no longer subject to federal tax. Changes to federal tax law in 2017 allow Native corporations to make contributions to a settlement trust using pre-tax dollars. This change reduces the federal government’s share of a Native corporation’s income, creating a cash savings that can then be used to fund benefit programs, like distributions.

What is a settlement trust?

Under the Alaska Native Claims Settlement Act (ANCSA), Sealaska can set up a special entity called a “Settlement Trust” that is legally separate from Sealaska and dedicated to providing benefits to shareholders and descendants. The purpose of a settlement trust is to provide for the health, education, cultural preservation and economic welfare of Alaska Native people and descendants who are the “beneficiaries” of the settlement trust.

In the past, Sealaska paid dividends to the shareholders directly. Now, Sealaska transfers money to the settlement trust, which is used to make distributions to shareholders.

I heard about the new Sealaska Settlement Trust. Where do I sign up?

There’s no need to sign up for anything or fill out any paperwork. Shareholders retain their shares in Sealaska, and are now also beneficiaries of the Sealaska Settlement Trust in equal proportion to the shares they own in Sealaska. For example, a shareholder who owns 100 shares in Sealaska now owns 100 units in the Sealaska Settlement Trust as well. Your distributions will be paid to you as usual and the experience should be seamless.

Common Terminology Associated with a Settlement Trust

Settlement trusts use different words for many of the concepts you’re familiar with as a shareholder or descendant of Sealaska.

What does “tax-free distributions” mean?

Shareholder distributions made through the settlement trust are not subject to federal income tax.

Shareholders may still have to pay state tax, though. In Alaska and Washington, where the vast majority of our shareholders reside, there is no state-levied personal income tax, so distributions from the settlement trust will be 100% tax free. Elsewhere, distributions could be taxed if the state where you live has personal income tax.

Shareholders of class A, B, and C shares will continue to receive ANCSA Section 7(j) distributions either directly from Sealaska or their village corporation and those amounts will still be taxable.

When did it go into effect?

Shareholders received their first distribution via the trust in the fall of 2021. The second trust distribution is scheduled for Friday, April 22.

How long have ANCs been using settlement trusts?

Settlement trusts are not new. They have been used by Native corporations in Alaska since the late 1980s and have been approved by shareholders of Ahtna Inc., Bering Straits Native Corporation, Calista Corporation, Cook Inlet Region Inc. and NANA Regional Corporation, along with many village corporations in our region including Goldbelt, Inc., Kootznoowoo, Inc., and Huna Totem.

In fact, Sealaska already has an established Elders’ Settlement Trust for one-time payments to shareholders of Class A, B and C stock when they reach the age of 65. The relatively new tax law, however, allows Sealaska’s new settlement trust to benefit all Sealaska shareholders and descendants year after year.

THE SETTLEMENT TRUST AND YOUR DISTRIBUTIONS

How does the Sealaska Settlement Trust impact my distribution?

The amount of the distribution is the same as it would have been without the settlement trust, and the process of determining the distribution is also unchanged.

- Sealaska’s board of directors meets each April and October to determine how much to pay out in a twice-yearly distribution following a defined dividend policy. (Read about how distributions are calculated)

- Once that announcement is made (on Friday, April 8 for this spring’s distribution), shareholders will be able to view their pending payment in com.

- The amount approved by the board for the spring distribution will be transferred to the Sealaska Settlement Trust. This functions as a separate bank account. Payments will be made from the Sealaska Settlement Trust account instead of the Sealaska corporate account as in the past.

- On Friday, April 22, payments will be processed. People who are signed up for direct deposit will receive their distribution electronically on the same day. Checks will be mailed the same day as well.

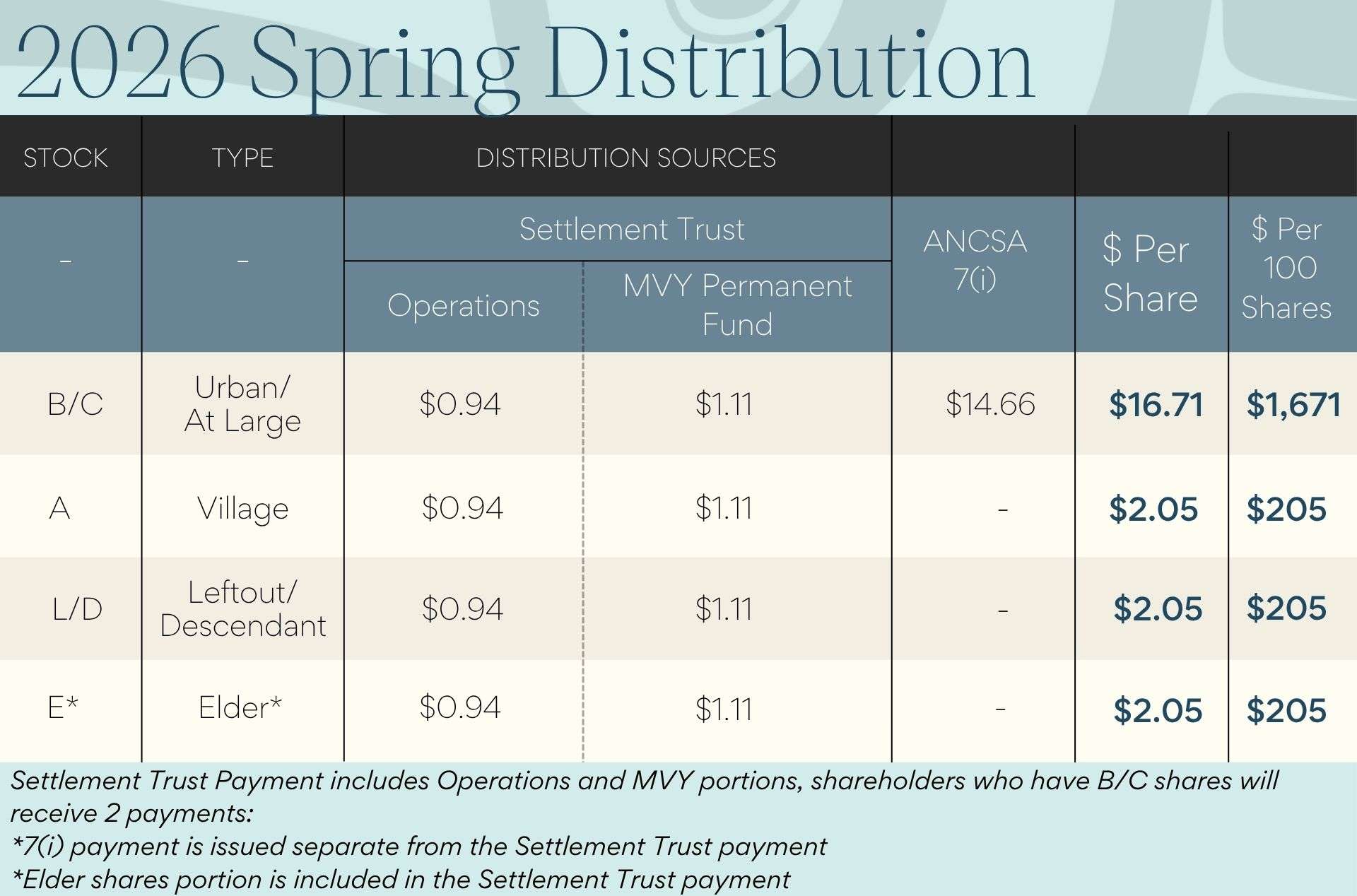

Attention Class B (Urban) and Class C (At-Large) shareholders:

Class B (Urban) and Class C (At-Large) shareholders receive Alaska Native Claims Settlement Act (ANCSA) Section 7(j) distributions directly from Sealaska (instead of from a village corporation, as is the case for Class A (Village) shareholders). Section 7(j) payments are not eligible to be transferred into the Sealaska Settlement Trust and will continue to be paid directly from Sealaska. Class B (Urban) and Class C (At-Large) shareholders will receive two separate payments from now on – distributions based on earnings from operations and the Marjorie V. Young Permanent Fund will be paid from the settlement trust; 7(j) payments will continue to be paid from Sealaska.

For Class B (Urban) and Class C (At-Large) shareholders, this means you will receive TWO direct deposits or paper checks, depending on how you receive your distributions. The direct deposits should occur one right after another, essentially simultaneously. Checks will be issued and mailed at the same time, but the mail-handling process may mean that these checks arrive on different days.

Because Class B (Urban) and Class C (At-Large) shareholders will still receive Section 7(j) payments from Sealaska, that portion of their distribution will still be considered taxable income for federal income tax purposes. You will continue to receive an IRS Form 1099 from Sealaska each January documenting these payments.

(Need a breakdown of Sealaska’s other classes of stock? Click here.)

I haven’t received my check yet – is this because of the settlement trust?

Payments from Sealaska accounts are processed out of a Wells Fargo processing center in Arizona, which Sealaska has used for the last 10 years. If your check is taking longer than usual to arrive, it could be due to new, slower delivery standards for first-class mail. What used to take up to three days may now take up to five days within the United States. Checks will be mailed on April 22, so it could take an additional week to receive them. If you want to receive your distribution payments faster, please sign up for direct deposit.

My check is a lot lower than usual. I thought the Sealaska Settlement Trust was supposed to save money. What happened?

If you are a Class B or Class C shareholder, you will probably notice that your distribution this spring is lower than normal. This has nothing to do with the Sealaska Settlement Trust. Payments from ANCSA Section 7(j) are down considerably due to the impact the pandemic had on commodities prices like oil, natural gas and certain minerals. Section 7(j) payments come from the natural resources revenue earned by other Alaska Native corporations and shared collectively under ANCSA Section 7(i). With prices for resources produced by other ANCs on the decline, we can expect to see payments from ANCSA Section 7(j) decrease as well.

Will shareholder benefits change with a settlement trust?

Dividend calculations and distributions are not changed by the settlement trust. Other non-cash shareholder benefits are not impacted by the settlement trust.

TRUST ADMINISTRATION

Who manages the settlement trust?

The settlement trust is managed by a 13-member board of trustees. The board of trustees is made up of all 13 members of Sealaska’s board of directors.

Is the board of trustees paid for governing the settlement trust?

There is no additional compensation paid to the board of trustees for its work. Trustees are members Sealaska’s board of directors and will not receive more than their scheduled compensation as a director.

How can shareholders influence the trust?

Because all members of Sealaska’s board are also trustees, a vote for a board candidate is a vote for a trustee. Sealaska will continue to survey shareholders on a regular basis to assess your priorities and ensure our benefit programs align with your values and concerns.

How do shareholders receive distributions from the settlement trust?

Distributions from the settlement trust are paid to shareholders the same way dividends prior to its adoption. When the board meets in April and October, they approve the distribution amount based on a formula that has not changed since the settlement trust was implemented. Shareholders receive their distribution based on how many shares they own and the class(es) of shares. With the settlement trust, once the board approves the total distribution amount from Sealaska, funds are transferred to the settlement trust and the trust issues distribution payments to shareholders. The main difference shareholders will notice is that with the settlement trust, shareholders won’t have to pay federal taxes on their distributions. For those who are not eligible for ANCSA Section 7(i) payments, this means you will no longer receive an IRS Form 1099 each year. (Shareholders who DO receive 7(i) payments will continue to be taxed on those payments as they cannot be routed through the settlement trust.)

Will shareholders lose shares with a new settlement trust?

If you have 100 shares of Sealaska stock, you now also own 100 units in the settlement trust. Your shares in Sealaska still exist, and can still be gifted or willed to someone else. For example, if you gifted 10 shares of Settlement Common Stock in Sealaska to your grandchild, your grandchild will receive those shares as well as 10 distribution-paying units in the settlement trust.

How does the Trust Agreement protect beneficiaries?

The trust agreement protects beneficiaries and guides the trustees. It requires that each trustee act in good faith, solely in the interests of the beneficiaries (shareholders), and with care, skill, prudence and diligence. Trustees are required to bring their attention, skill and focus to the job of managing the trust, just as Sealaska directors are required to act in good faith on behalf of shareholders. The trust agreement may be amended, but only in limited circumstances. Because the trust is intended to last indefinitely, the agreement gives trustees the flexibility to amend the trust as needed based on future circumstances. Shareholders will receive an annual report from the settlement trust along with the Sealaska annual report each year in late April / early May.

How does the Trust Agreement protect beneficiaries?

The trust agreement is the legal and financial description of what the trust is supposed to do and outlines the responsibilities of the trustees. It is designed to protect the beneficiaries and guide the trustees. The trust agreement requires that each trustee act in good faith, solely in the interests of the beneficiaries (shareholders), and with care, skill, prudence and diligence. Trustees are required to bring their attention, skill and focus to the job of managing the trust, just as Sealaska directors are required to do on behalf of shareholders. Because the trust is intended to last indefinitely, the agreement gives trustees the flexibility to amend the trust as needed based on future economic circumstances. The trust agreement identifies certain types of changes that require more than “standard” approval by the appropriate body – the Board of Trustees and/or the Sealaska Board of Directors.

Latest News

2026 Sealaska Election Results

Posted 6/29/2026At Sealaska’s 53rd Annual Meeting in Aangóon (Angoon), the Inspector of Elections certified the results of the 2026 election.

Sealaska tackles massive project to protect Juneau-area communities from catastrophe

Posted 6/17/2026

Sealaska Announces $29.7 Million Spring Distribution to Shareholders

Posted 4/10/2026

Sealaska Board of Directors April Meeting Recap

Posted 4/10/2026The Sealaska Board of Directors met on April 10, 2026, and conducted key governance actions while receiving updates on shareholder services, shareholder development, natural resources and regional economic development.

Notice of Sealaska's 53rd Annual Meeting of Shareholders

Posted 2/12/2026The 2026 Sealaska Annual Meeting of Shareholders will be held on Saturday, June 27, in Angoon, Alaska. This year’s meeting will take place at the Angoon Elementary Gym, located at 500 Big Dog Salmon Road, Angoon, AK 99820.